DISCLAIMER: THEDREAMTEAMHAWAII.COM IS NOT THE OFFICIAL WEBSITE FOR THE CENTRAL ALA MOANA CONDO PROJECT. THE PROPOSED PROJECT IS BEING DEVELOPED BY SAMKOO HAWAII LLC. ALL INFORMATION IS SUBJECT TO CHANGE.

The Central Ala Moana built by SamKoo Pacific LLC will be SamKoo's second tower located on the corner of Kapiolani Boulevard and Kona Iki Street. This Central will be a 43 story building and will feature 512 units. They will set aside 60% (310 units) towards affordable housing and the other 40% (202 units) will be sold as market units. Construction to start 2nd quarter of 2019.

The Central Ala Moana built by SamKoo Pacific LLC will be SamKoo's second tower located on the corner of Kapiolani Boulevard and Kona Iki Street. This Central will be a 43 story building and will feature 512 units. They will set aside 60% (310 units) towards affordable housing and the other 40% (202 units) will be sold as market units. Construction to start 2nd quarter of 2019.

Register Your Interest To Be Kept Up To Date

Artist Rendering of The Central Ala Moana

|

The Central Ala Moana by SamKooUnit Breakdown: 512 units (310 Affordable & 202 Market)

MAINTENANCE FEE: Est $0.69 per sq. ft. Includes Sewer, Water, Cable, and Internet MARKET PRICES: $580,000 - $1,398,000 (No Market Studios) SOLD OUT

|

Typical Tower Floor Plan

The Central Ala Moana will typically have 13 units per floor. On the higher floors some of units combine to make larger units. The typical level consists of:

- 3 Studios (grey),

- 4 One-bedrooms (orange),

- 5 Two-bedrooms (blue), and

- 1 Three-bedroom (green).

|

|

Mountain and Ocean ViewsThe Central Ala Moana will have a mix of Mountain and Ocean view units. The Ocean side will definitely be the more costly of the two sides but will boast incredible Ocean Views overlooking Magic Island, Ala Wai Boat Harbor, and Ala Moana Beach. This side will most likely be the more popular of the two because the only thing in front is Park Lane and Ala Moana Shopping Center and there is less of a chance that something will be built in front of you.

|

|

|

|

AmenitiesThe Central Ala Moana will be a higher grade building compared to their first project Kapiolani Residence. The Central Ala Moana will have the following amenities:

|

|

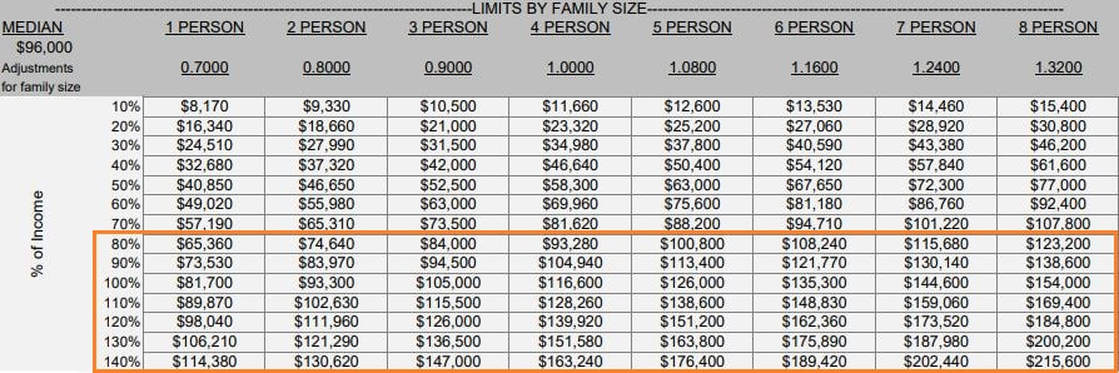

Affordable Housing Income Limits

There will be 310 affordable housing units in The Central Ala Moana. This building will be a little different from it's predecessor Kapiolani Residence. This time around buyers will be allowed to make up to 140% of the 2018 area median income (Kapiolani Residence was up to 120%). Per HHFDC the area median income will be classified by family size and you may use the table below see which bracket you fall under. The important thing to remember is that you NEED to be within the 80% to 140% AMI range.

Approved Project Lenders

Part of the application will be to get a project pre-qualification letter from one of the following lenders. It is highly advised to start as soon as possible as they will get busy the longer you wait. Remember, you do not need to use the person you pick for the loan. You can use whoever you want even if the lender or bank isn't listed as a project lender. If you need advice on picking a lender feel free to reach out to us.

**For a clearer/zoomed in picture, please see the attached jpg file for each approved project lender**

|

|

|

|

|

|

| ||||||||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Frequently Asked Questions

The Hawaii Housing Finance and Development Corporation (HHFDC) is the primary agency charged with overseeing affordable housing, financing, and development in Hawaii.Their website is http://dbedt.hawaii.gov/hhfdc/

1. Allows eligible and qualified applicants to purchase at below market prices

2. Homebuyers have an opportunity to live in town at a brand new development that fits their budget

3. There are no asset limits

4. Gifting and co-signing provide an opportunity for homeownership.

5. No household limitations (subject to the City and County of Honolulu ordinances)

6. SAE is a percentage of appreciation and can be paid off at any time after close

1. Sign up to receive updates on when the Application Packet will be released

2. Fill out the Application Packet and meet with a Lender for pre-qualification

3. Return the completed packet to the Sales Center

4. HHFDC First Review – Review of applications to determine eligibility

5. Public Drawing

6. HHFDC Second Review – Assignment of Property Selection Number (PSN)

7. Unit Selection & Contract Signing

Affordable Housing is for buyers earning 140% and below of the Area Median Income.

The HHFDC will determine eligibility based on the information you provide in your Application Packet, including the following:

1. US Citizen or permanent resident alien

2. At least 18 years of age

3. Resident of the State of Hawaii who currently resides in the State of Hawaii

4. Shall physically reside in the unit purchased

5. Does not own a majority interest (more than 50%) in a fee simple or leasehold property anywhere in the world

6. Has sufficient gross income to qualify for the loan to finance the purchase

The buyer will need to provide $500 at contract signing and the remainder of 5% minus the $500 after 30 days.

The owner is required to be an owner occupant for 10 years. The buyback program gives the HHFDC the first option to purchase the property in the event of a sale or transfer during the first 10 years of ownership. Owner occupancy is a requirement during this period. The restriction automatically terminates at the end of 10 years from the recording date.

SAE is Shared Appreciation Equity. This is the sharing of the property’s net appreciation with the HHFDC in exchange for the buyer’s opportunity to purchase at below market prices. The SAE percentage is calculated prior to closing and once determined, does not change.

The SAE must be paid when the property is sold, transferred or rented. Owners also have the option of paying it off at any timeafter closing.

The HHFDC will require documentation to support the buyer’s application. Some examples are: current year tax returns, W-2, 2 months of paystubs, and a letter of pre-qualification from a Lender. Lenders will have different requirements to determine loan pre-qualification.

The formula is: Original Fair Market Value (determined by appraisal prior to closing), minus Original Purchase Price, divided by Original Fair Market Value, and rounded to the nearest one percent.

Yes, you may select from any available unit that you are eligible (determined by HHFDC) and qualified (as determined by Lender)to purchase.